The Institutional Limited Partners Association has released a universal, standardised limited partnership agreement template called the ‘Model LPA’, in a first for the private equity industry.

“The banking industry uses standardised documentation (called ISDAs),” says MJ Hudson partner and LPA Task Force member Eamon Devlin “so there’s no reason why private equity can’t do the same.”

While ILPA claims that the template will be of benefit to both LPs and GPs, it has been met with “some resistance from a number of parties” within the industry, according to Devlin. Here are some of the key changes in the document, discussed by Devlin and ILPA senior policy counsel Chris Hayes.

Co-investing (9.3)

“There are two big changes here,” says Devlin. First, the clause calls for GPs to give notice to each LP of any co-investments elsewhere in the fund. Second, co-investors would be liable for a pro-rata share in broken deal fees where co-investments fall through.

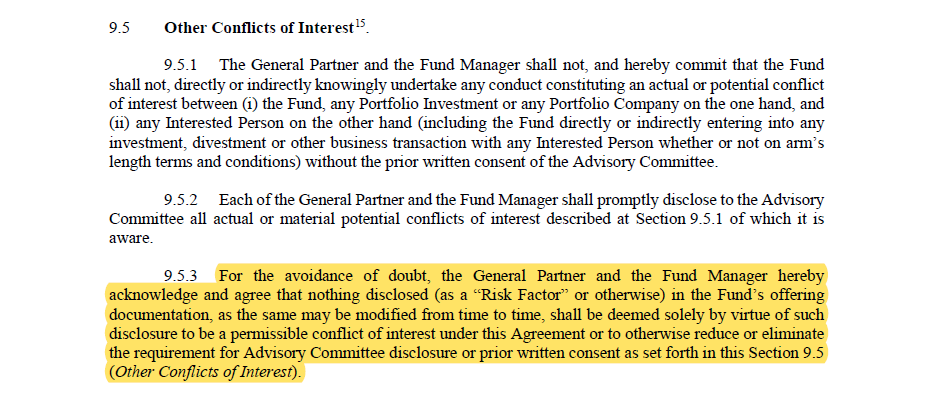

Conflicts of interest (9.5)

“It is important that conflicts are brought to the limited partnership advisory committee when they arise, rather than trying to pre-clear all those potential conflicts,” says Hayes, speaking on a podcast with Private Funds CFO. Presenting LPs with too many potential conflicts of interest for pre-clearance during the investment period makes the disclosures “less meaningful,” and dealing with conflicts as they arise creates “a better process for alignment between the GP and the LP.”

Removing a GP (10.1)

As is standard in most LPAs, LPs have the right to remove the fund manager in the event of removal conduct, but ILPA’s version also allows the opportunity for LPs to remove the GP without cause, as long as 75 percent of them vote in favour of the removal. According to Devlin, this sort of provision is “less common in US funds.”

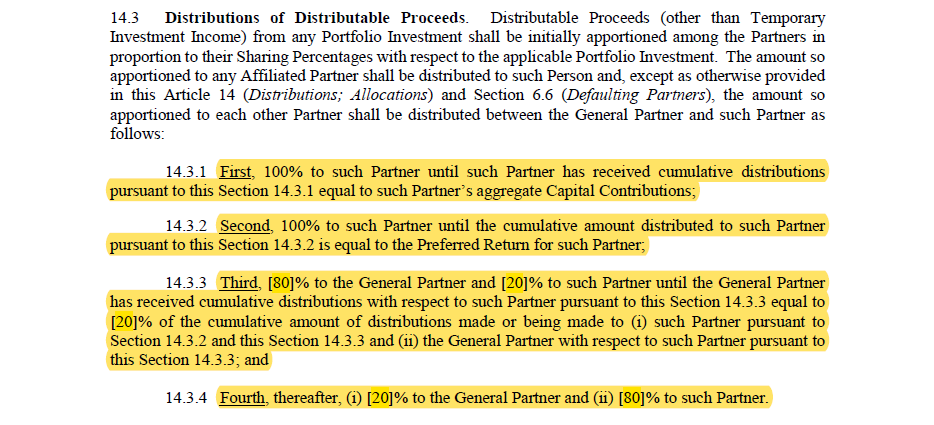

Waterfall calculations (14.3)

“A lot of US buyout funds have a deal-by-deal waterfall, where carry depends on the outcome of each individual deal, but this model doc is trying to make the fund-as-a-whole method more common,” says Devlin. “This is arguably the most important clause, and one that took a lot of negotiation internally.” Law firm Clifford Chance described this in a note to clients as “a useful reminder of the continuing disconnect between ILPA and, on this issue in particular, the US sponsor community.” ILPA does plan to release a deal-by-deal waterfall plan “down the line,” adds Hayes, “just because of its prevalence in the marketplace.”

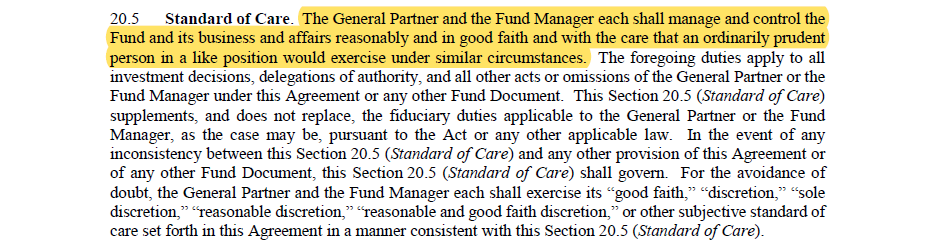

Fiduciary duty (20.5)

The LPA includes a nod to fiduciary duty – an area where trends are, according to Hayes, “going in the wrong direction.” ILPA members have been expressing concern about GPs “contracting away” fiduciary duty, says Hayes. “It is core that there be a duty of loyalty and a duty of care.”

Identifying LPs (20.7)

“LPs have certain governance rights, and if they don’t know who their fellow LPs in the fund are, they may not be able to exercise those governance rights,” says Hayes. However, this clause only requires the list of LPs to be available to the investor base. “This doesn’t mean that we think it should be disclosed to the public at large – this is about internal fund governance.”

If you do not receive this within five minutes, please try to sign in again. If the problem persists, please email:

If you do not receive this within five minutes, please try to sign in again. If the problem persists, please email: